Beyond the GPU: What Nvidia and Micron Reveal About the Next Phase of AI Value Creation

Category: AI, Technology & Value Creation

Written by: Dr.Baron W. De Rothschild 08/06/2026

The AI boom is moving beyond chips into memory, infrastructure, supply chains, and capital allocation.

AI is no longer only a software story. Nvidia has become the most visible name in accelerated computing, but the next phase of AI value creation depends on the wider infrastructure behind it: memory, storage, data centres, power, cooling, and supply chain capacity. Companies such as Micron show why high-bandwidth memory is becoming central to AI performance and why business leaders need to understand the full value chain before making investment decisions.

Key developments include:

- AI demand is increasing the importance of physical infrastructure, not just software.

- Nvidia’s growth is creating demand across the semiconductor and data centre ecosystem.

- Memory suppliers such as Micron are becoming more strategically important.

- Capital allocation decisions around AI are becoming more complex.

- Companies need a clear commercial use case before investing in AI tools or infrastructure.

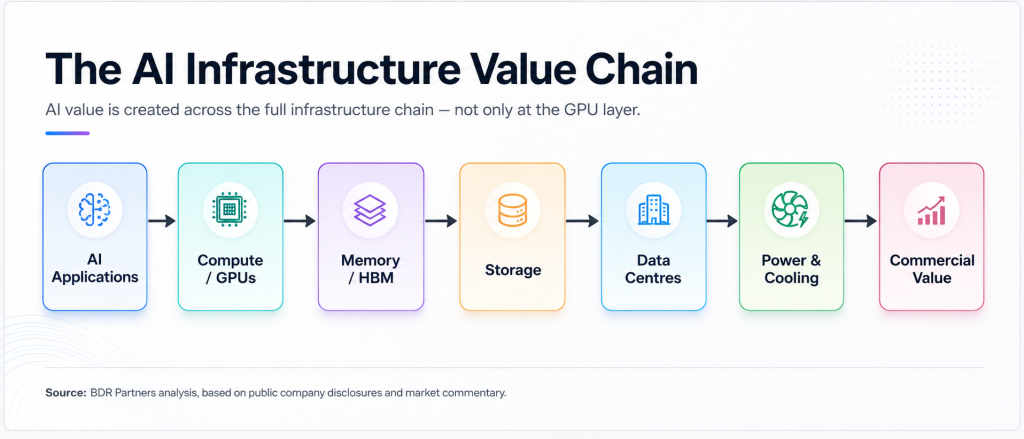

The figure above makes the central point clear: AI value is now created across an entire infrastructure stack, not in one component alone. Current announcements from Nvidia, Micron, TSMC and other large infrastructure players all point in the same direction. This is no longer a narrow software story. It is a broader build-out of compute, memory, networking, storage, data-centre capacity and power.

AI is becoming an infrastructure market

AI is increasingly being shaped by the economics of physical infrastructure. Nvidia’s latest quarterly results show how far the market has moved in this direction: data-centre revenue reached $75.2 billion, with growth now extending across hyperscalers, AI clouds, industrial deployments and enterprise environments. TSMC is expanding advanced packaging and manufacturing capacity in response to what it describes as strong multi-year AI-related demand. At the same time, the International Energy Agency expects electricity supplied to data centres globally to rise from around 460 TWh in 2024 to more than 1,000 TWh by 2030. The point is straightforward. AI is no longer only about models and applications; it is also about chips, packaging, storage, networking, sites, power and cooling.

That changes how business leaders should read the market. Competitive advantage will not come from model access alone. It will come from securing capacity, choosing the right partners, understanding where bottlenecks sit and converting technical capability into reliable commercial output. As Nvidia’s Vera Rubin platform moves into volume production through a network of hundreds of ecosystem partners across hundreds of factories, the market is becoming broader, more capital intensive and more operationally complex.

Why memory matters

Memory now sits much closer to the centre of AI economics than many businesses appreciate. Faster processors only create value if they can be fed with data quickly enough, and that is why high-bandwidth memory has become strategically important. Micron is already shipping HBM4 designed for Nvidia Vera Rubin, with bandwidth above 2.8 TB/s and better power efficiency than the previous generation. In Micron’s own positioning, AI-era memory and storage are no longer background components; they are strategic assets.

The commercial implication is significant. Faster memory affects how well advanced reasoning, multimodal and agentic systems perform, and it influences how much context and activity can be supported efficiently. Nvidia’s own Blackwell architecture notes that memory capability directly affects the performance and scale of next-generation models, while Micron’s HBM roadmap is now tied to live AI platforms rather than abstract future demand. In practical terms, the AI race is no longer only about who builds the leading processor. It is also about who can supply the memory, packaging and storage that allow those processors to deliver real performance.

The capital allocation challenge

Once AI becomes infrastructure, capital allocation becomes more demanding. The largest buyers are no longer spending on servers alone. Microsoft said capital expenditure in its latest quarter was $31.9 billion, with roughly two thirds spent on short-lived assets such as GPUs and CPUs, while finance leases were mainly tied to large data-centre sites. Alphabet has described a similar split, with most technical infrastructure spending going into servers and the balance into data centres and networking equipment, while guiding to $175 billion to $185 billion of capital expenditure in 2026. TSMC and Micron are making parallel decisions in advanced packaging, manufacturing footprint and memory capacity as AI demand stays strong.

Most organisations will never spend at that scale, but the underlying question is the same. Where should capital go first: cloud capacity, internal data foundations, workflow automation, customer-facing applications or new operating capability? There is rarely room to do everything at once. The businesses that create value will be the ones that sequence investment properly, know where constraints sit and stay disciplined on return rather than following the headlines. In the current market, availability, pricing, depreciation and operating costs all matter as much as technical ambition.

What business leaders should do now

Business leaders should start by defining the commercial problem before selecting the technology. In practice, that means being specific about whether AI is expected to increase revenue, reduce cost, improve decision speed, strengthen service or lower risk. The next step is to map dependency across the stack: model access, cloud providers, compute and memory availability, data quality, systems integration, governance and, where relevant, hosting and energy considerations. Only then should management approve spend, because only then can finance and operations test whether the case is robust.

Execution matters just as much as the initial decision. The stronger programmes now have clear ownership, measurable milestones, controls around security and data, and a direct link to margin, productivity or growth. The weaker ones still treat AI as an isolated experiment sitting outside the business. In the current market, that is rarely enough. The companies moving fastest are not simply buying more technology; they are making sharper decisions about where AI genuinely improves performance and where investment can be justified commercially.

BDR Partners’ view

The AI opportunity should not be reduced to adopting a tool or launching a pilot. Value is moving across a wider stack of compute, memory, storage, networking, data-centre capacity and energy, and that shift is changing both competitive dynamics and investment priorities. For leadership teams, the task is to decide where to place capital, where to partner, how to manage exposure and how to translate technical capability into growth, margin improvement or stronger operating performance.

BDR Partners helps businesses do that with clear strategic thinking, disciplined investment choices and transformation work tied to measurable commercial outcomes.